The “Mirror” Rule You Didn’t See Coming

Most pet owners understand the “Bilateral Exclusion” when it comes to knees.

- Rule: If your dog tears the Left ACL, the insurance company excludes the Right ACL automatically because they assume the dog has “bad knees.”

But here is the question that is costing Frenchie owners thousands of dollars:

Does this rule apply to their nose?

Brachycephalic Obstructive Airway Syndrome (BOAS) often involves Stenotic Nares (pinched nostrils). Since your dog has two nostrils, some aggressive insurance adjusters are now using the “Bilateral” clause to deny breathing surgeries.

In this guide, we expose the “Nostril Loophole”—and how to make sure your BOAS claim doesn’t get rejected on a technicality.

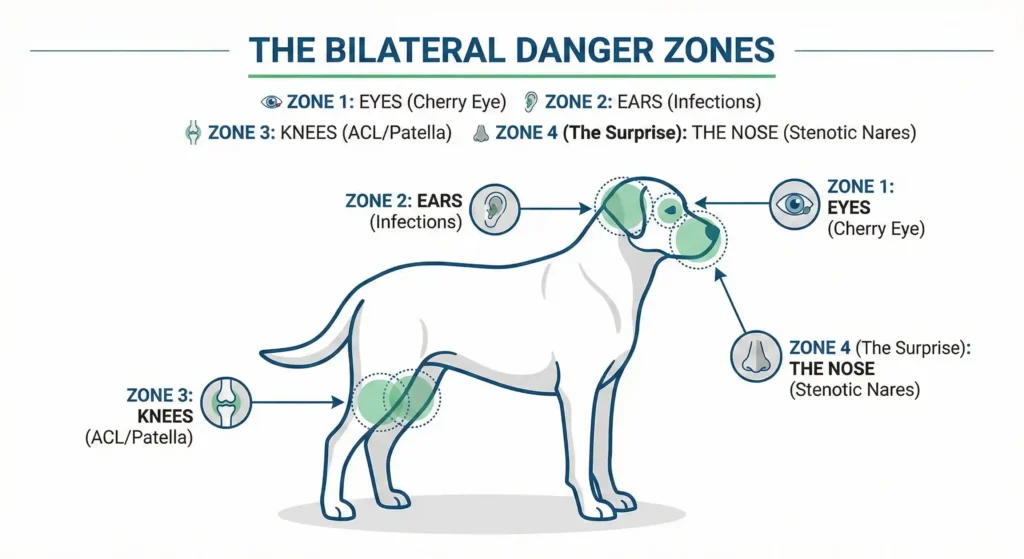

Stenotic Nares: The $2,500 “Pre-Existing” Trap

To understand the insurance trap, you first need to understand the anatomy.

Stenotic Nares are when the nostrils are pinched shut, forcing the dog to breathe through a tiny slit.

If you take your 6-month-old puppy to the vet and the vet notes: “Mild narrowing of left nostril,” you might think nothing of it.

Two years later: Your dog needs full BOAS surgery (Palate + Nares).

The Denial: The insurer denies the entire surgery (both nostrils and often the palate too) claiming that because one nostril showed signs early, the entire respiratory system is a “Bilateral Pre-Existing Condition.”

Is BOAS Technically Bilateral? (The Expert Answer)

The short answer: It’s Complicated.

- The “Good” Insurers: Treat BOAS as a Systemic Syndrome. They look at the whole picture. If the dog had no breathing issues before the policy, they cover it.

- The “Bad” Insurers: Treat Nares as Bilateral Organs (like eyes or knees). If any part of the nose looked “tight” in a puppy exam, they exclude the entire nose for life.

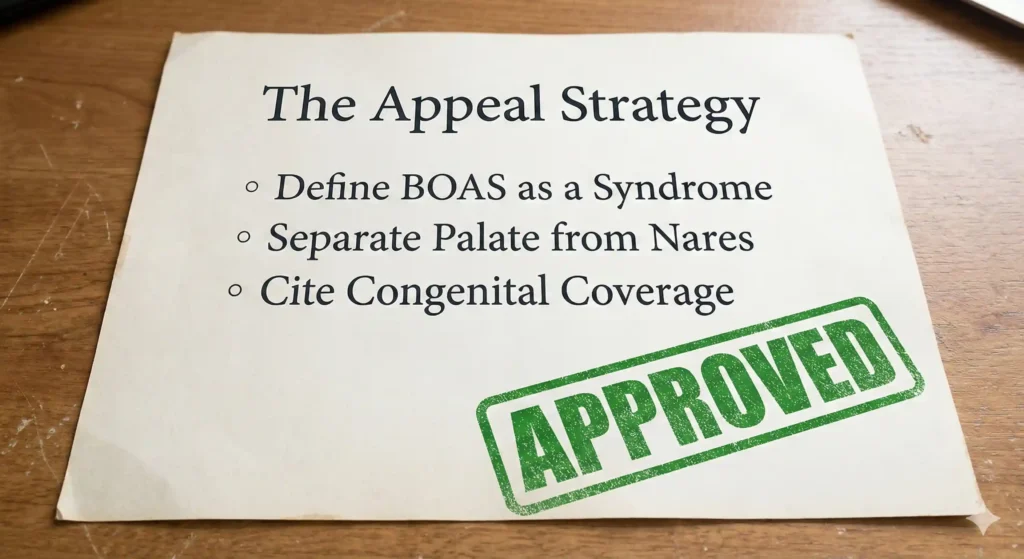

How to Fight Back (And Win)

If your claim is denied based on the “Bilateral Nostril” argument, do not accept it. Here is your battle plan.

1. The “Syndrome” Defense

Argue that BOAS is a Syndrome, not a single organ failure.

- Your Argument: “Stenotic Nares are just one symptom of a larger syndrome (BOAS). My dog’s elongated soft palate (which is causing the choking) is NOT bilateral—it is a single central structure. Therefore, the bilateral exclusion cannot apply to the throat surgery.”

2. The “Anatomical Deviation” Defense

Ask your vet to write a letter stating: “The patient’s condition is a congenital anatomical malformation of the skull, not a degenerative bilateral disease like arthritis or cruciate disease.”

- Many policies have different rules for “Congenital Traits” vs. “Bilateral Diseases.” Shifting the category can get the claim paid.

3. Get a “Review” Before Surgery

Never go into surgery blind. Ask your insurer for a “Medical History Review” specifically asking: “Are there any bilateral exclusions on my dog’s respiratory system based on past records?” Get the answer in writing.

Conclusion: Don’t Let Them Split Hairs

Insurance companies love to split hairs to save money. They will try to tell you that a left nostril issue predicts a right nostril issue, just so they don’t have to pay for the laser surgery that helps your dog breathe.

Know the terms. Read the “Bilateral” clause in your policy today. If it doesn’t explicitly exclude “Respiratory System,” you have a fighting chance.

Frequently Asked Questions (FAQs)

-

Does Trupanion cover BOAS surgery?

Trupanion generally covers BOAS if no signs were present before enrollment. However, they are strict about “breed-related conditions” if they were noted in early exams. Always check your specific policy waiting periods.

-

Is a Soft Palate considered Bilateral?

No. The Soft Palate is a single structure in the center of the throat. Insurers cannot use the “Bilateral Exclusion” on the palate itself, but they might try to link it to the Nares (nostrils) to deny the whole claim as a “Respiratory Complex.”

-

Can I fix just the nostrils to save money?

You can, but it is rarely recommended. The Nares and the Palate work together. Fixing only the nose is like opening a window in a house where the hallway is blocked. Most vets recommend doing both (Nares + Palate) at the same time for one anesthesia fee.